Introduction

Tax returns are essential documents that individuals and businesses must file annually to report their income, expenses, and other financial information to the government. This guide aims to provide a clear understanding of tax returns, the filing process, benefits, and common questions surrounding them.

Determining the source of your income is important for understanding your tax obligations in Thailand. Thai tax residents are now obligated to include such assessable income when calculating their annual assessable income for the calendar year they remit the overseas income into Thailand (this taxation is subject to applicable DTAs and other exemptions). This shift in policy, effective from January 1, 2024, requires individuals to carefully assess whether their income is classified as Thai-sourced or foreign-sourced.

With recent changes in tax regulations, including Departmental Instruction No. Por. 161/2566 issued by the Revenue Department, the implications for tax residents have become more significant.

In this blog post, we will explore how to identify the source of your income and the associated tax implications.

Key Points

- As of January 1, 2024, Thai tax residents must include foreign-sourced income remitted to Thailand in their annual assessable income

- Determining the income source is for tax obligations; Thai-sourced income is taxable for both residents and non-residents in the year it’s received.

- Foreign-sourced income may be exempt from Thai personal income tax under certain conditions, such as Double Tax Agreements or holding specific Long-Term Residency visas.

- Thai-sourced income includes earnings from employment, business, investments, and capital gains within Thailand, regardless of where payment is made.

- Special tax rates apply to certain groups, including a 17% flat rate for LTR Highly-Skilled Professionals and EEC visa holders, and a 15% rate for qualifying International Business Center employees.

What is a Tax Return?

A tax return is a formal statement filed with a tax authority that outlines an individual’s or entity’s income, expenses, and other pertinent financial information for a specific tax year. The primary purpose of a tax return is to calculate the amount of tax owed or the refund due. Tax returns can vary based on the type of income earned, deductions claimed, and credits applied.

Why is it Important to Determine Whether Income is Foreign or Thai Sourced?

On September 15, 2023, the Director General of Thailand’s Revenue Department issued Departmental Instruction No. Por. 161/2566. This instruction, titled “Payment of Income Tax under Section 41, Paragraph 2 of the Revenue Code,” redefines the tax liability of Thai tax residents who earn income from foreign sources in a given calendar year and repatriate this income to Thailand in any subsequent calendar year.

Under this new interpretation, Thai tax residents are now obligated to include such assessable income when computing their annual assessable income for the calendar year they remit the overseas income into Thailand. In essence, this means that Thai tax residents must fulfil their Thai personal income tax obligations on such overseas income, even if the repatriation occurs in a different calendar year from the one where the overseas income was initially earned. However, the tax liability of this income is subject to any relevant double taxation agreements and other applicable exemptions e.g. being a holder of an LTR visa (except the LTR for Highly Skilled Professionals)

It is important to note that these new regulations came into effect on January 1, 2024.

For more information, please see here.

What are the Tax Obligations for Income in Thailand?

Being able to determine what is considered Thai income is an important consideration when it comes to preparing and filing your annual tax returns in Thailand.

Thailand’s personal income tax laws clearly state an individuals tax obligations owed from receiving Thai sourced income. Regardless of nationality or tax residence status, individuals who generate income from sources within Thailand are subject to personal income tax on that income in the same calendar year it is received.

An individual’s tax residence status does not affect their personal income tax obligations in Thailand. Thai personal income tax applies to Thai sourced income regardless of whether the recipient is a Thai resident or non-resident for tax purposes. An individual is considered a Thai tax resident if they stay in Thailand for at least 180 days within a calendar year. This applies regardless of nationality or visa status.

Non-residents are subject to Thai personal income tax on their Thai sourced income in the same manner as Thai residents. Tax residents are subject to all income earned or remitted to Thailand (subject to certain exemptions such as double tax agreements and if the holder has a LTR visa etc).

It is important to note that the tax rates and filing requirements are the same for both residents and non-residents.

How to Determine Thai-Sourced Income?

In Thailand, Thai-sourced income refers to income that comes from or is earned from activities or assets within Thailand. Key types of Thai-sourced income include:

Income from Employment: Earnings earned from work undertaken in Thailand, irrespective of where the payment is made e.g. being paid by a company or person outside of Thailand.

Income from Business: Revenue and income earned from any form of trade, business, or professional activities conducted in Thailand.

Income from Investment: Income earned from dividends, interest, royalties, or rent from Thai sources or assets within Thailand.

Capital Gains: Income earned from profits from the sale or transfer of assets in Thailand, for example, gains made from selling real estate.

Please note that even for non-residents (those who stay in Thailand for less than 180 days per year), any income derived from Thailand is subject to Thai taxation.

How to Determine Foreign-sourced Income?

Income earned from the activities mentioned above can also be considered foreign-sourced income and potentially subject to tax if:

- The business activities take place outside of Thailand.

- The individual is a Thai resident (spends over 180 days in Thailand per year)

- The individual remits income into Thailand

Thai tax residents are liable to pay tax on income from sources in Thailand as well as foreign sources brought into Thailand, whereas non-tax residents are subject to tax only on Thai-sourced income.

Foreign sourced income may be exempt from Thai PIT if the following can be applied:

Income Earned Before December 31st 2023

Any income remitted to Thailand from abroad that was earned before December 31st 2023 will not be subject to the new income tax rules.

Double Tax Agreements

Thailand has entered into numerous DTAs with various countries. These agreements can help prevent double taxation on income earned abroad. If a taxpayer qualifies for benefits under a DTA, they may be able to exempt or reduce the tax liability on foreign income. For more information about DTAs, please see here.

Long Term Residency Visa

Holders of the Long-Term Residency (LTR) visa in Thailand are exempt from Thai personal income tax on foreign-sourced income, even if they bring that income into Thailand. This exemption applies to three categories of LTR visa holders: Wealthy Global Citizens, Wealthy Pensioners, and Work From Thailand Professionals. However, they must comply with specific conditions set by the Office of Board of Investment (BOI) to maintain this exemption.

Please note, holders of the LTR for Highly skilled professionals are not eligible for this exemption and instead receive a flat PIT rate of 17%

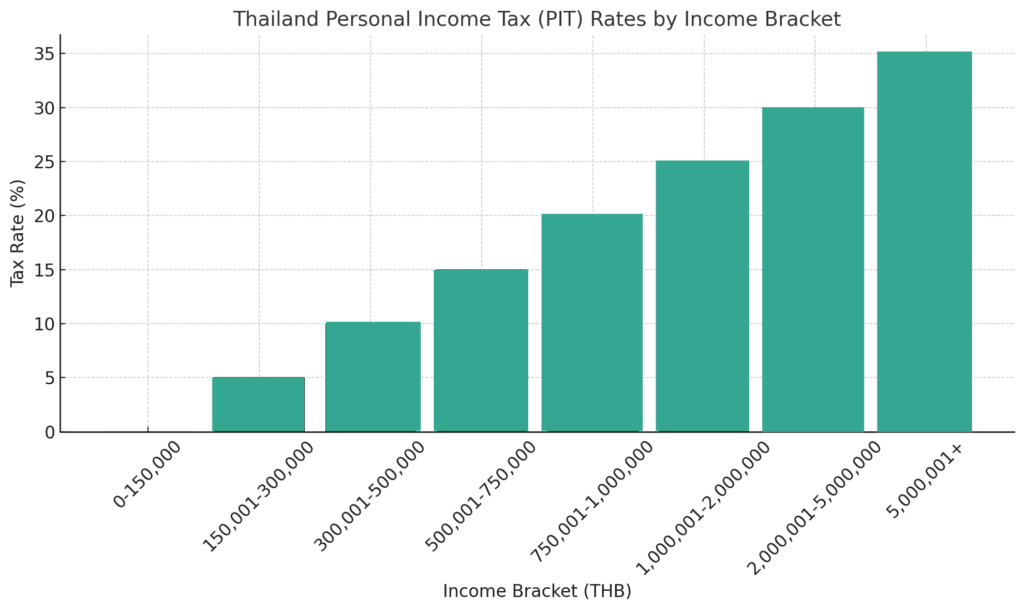

What are the Personal Income Tax Rates for Income in Thailand?

Thailand makes use of a progressive tax system for personal income tax, the rates of taxation can be seen below:

Please note, there are special rates of tax awarded to the following:

Holders of the Long-Term Resident (LTR) Visa

Holders of the Long-Term Resident (LTR) visa for Highly-Skilled Professionals enjoy a flat personal income tax rate of 17%.

Holders of the Eastern Economic Corridor (EEC) Visa

The EEC visa, introduced to attract specialists and executives in targeted industries, also provides a 17% flat tax rate on personal income.

Employees of an International Business Center (IBC)

Employees working for companies designated as International Business Centers (IBCs) may also benefit from a reduced flat tax rate of 15% on their income. To qualify, employees must meet specific criteria set by the Revenue Department, including being employed by an IBC engaged in targeted industries.

Returning Thai Professionals

In an effort to encourage highly skilled Thai nationals to return to Thailand, qualifying returnees will be eligible for a flat PIT rate of 17%

Our Thoughts

As the landscape of foreign income taxation in Thailand undergoes a significant shift, tax residents need to adapt to the upcoming changes.

For those who this isn’t possible, leveraging Double Tax Treaties where possible becomes vital for international tax planning, offering relief by crediting taxes paid abroad. Long-Term Residency visa holders enjoy exemptions, and our advisory services provide tailored solutions, guiding clients through these changes with expertise in strategic income management and comprehensive support. Looking for an Accounting firm in thailand? contact us for a consultation with one of our tax experts.