TL;DR

Bookkeeping services are recommended for all Thai companies, including dormant and foreign-owned businesses. Professional support helps manage CIT, VAT, payroll, withholding tax, audits, BOI obligations, director liability, and visa and work permit renewals.

Introduction

Foreign business owners are highly recommended to consider bookkeeping services in Thailand shortly after the company incorporation, regardless of whether a company is actively trading or dormant, in order to make sure they comply with all the mandatory accounting and tax filing requirements.

All registered Thai companies, and especially those with foreign ownership that are generally subject to additional scrutiny from the Thai authorities, are required to maintain proper bookkeeping in line with Thai accounting and tax regulations. This obligation applies even where a company has little or no commercial activity. Dormant companies must still record any transactions, prepare annual financial statements, and submit statutory filings, making bookkeeping and tax compliance in Thailand an ongoing legal responsibility rather than a one-off administrative task.

Bookkeeping for foreign-owned companies is an important consideration for foreign investors and business owners as the accounting and language requirements are significantly different to other jurisdictions.

For this reason, many businesses engage professional bookkeeping services in Thailand to help companies apply local rules correctly and consistently. While outsourced bookkeeping in Thailand reduces the risk of errors accumulating over time they also provide a practical way to maintain compliance whether the company is active, scaling, or temporarily inactive.

Key Points

- Bookkeeping services for foreign-owned companies are a compliance function, not simple data entry.

- Foreign ownership increases scrutiny from tax, audit, and immigration authorities.

- Accurate, timely bookkeeping under Thai standards is mandatory.

- Bookkeeping errors can affect tax filings, work permits application an renewal, BOI status and director liability.

- Professional bookkeeping reduces long-term risk and supports stable operations.

Why Bookkeeping Is Different for Foreign-Owned Companies

Bookkeeping is a very important part of running a business in Thailand. All companies in Thailand, whether or not they engage in business, are subject to mandatory accounting and tax filing requirements. These requirements apply equally to both operating businesses and dormant companies and form the basis of Thai bookkeeping compliance.

For foreign investors, this makes professional bookkeeping services in Thailand particularly important, as bookkeeping services for foreign-owned companies in Thailand must satisfy the local accounting standards, tax rules, VAT, payroll, and withholding tax obligations.

As a business owner, it is therefore essential to understand your ongoing bookkeeping and tax compliance responsibilities. This is especially relevant for company directors, as both the company and its directors may be held liable for non-compliance, with potential implications for audits, penalties and immigration status (visa renewals).

Read more:

How to Complete the Annual Closing Process for Company Accounts

Are foreign businesses subject to increased bookkeeping scrutiny?

Foreign-owned companies in Thailand are not automatically subject to increased scrutiny if they are properly structured, operate within their registered scope of activities, and comply with all tax and statutory filing obligations. However, in practice, certain activities commonly associated with foreign investors tend to attract closer review due to past abuses.

Real-estate-related structures are a good example. When a company owns land that would otherwise be restricted to foreigners under the Land Code, the presence of foreign shareholders usually leads to additional scrutiny. Authorities will look at the substance of the structure, the source of funds, and whether the company carries out genuine business activities. In this context, weak or inconsistent accounting records significantly increase risk.

The same applies to BOI-promoted companies. While BOI promotion allows 100% foreign ownership and provides tax incentives, it also limits permitted activities. BOI companies are frequently audited to verify that operations remain within the approved scope and that tax exemptions are correctly applied. Accounting and bookkeeping are often central to these reviews.

Finally, foreign-owned exporters and service companies applying 0% VAT or claiming high VAT credits commonly trigger VAT audits. These audits focus on invoices, contracts, and transaction substance. Poor bookkeeping or incomplete documentation can easily result in denied refunds and penalties.

In short, foreign businesses are not scrutinised because they are foreign, but because their structures, activities, or tax positions are more sensitive. In these cases, solid bookkeeping is not just a compliance exercise, it is a risk-management tool.

Read more:

BOI Accounting, Reporting and Compliance Requirements

Real Estate Companies in Thailand, Accounting and Tax Challenges

The link between bookkeeping, immigration, and director responsibility

For foreign-owned businesses, bookkeeping services can help ensure security and compliance in relation to immigration matters. When applying for or renewing your Non-immigrant B (business) visa Immigration authorities will request up-to-date financial statements, payroll records, VAT filings, and proof of tax payments when reviewing visa renewals, work permits, and director registrations.

Where Thai bookkeeping compliance is incomplete or inconsistent, applications can be delayed or refused.

Directors also carry personal liability under Thai law in relation to accounting non-compliance. Errors in filings prepared through inadequate accounting services in Thailand can expose directors to penalties and additional scrutiny. Where directors fail to meet their statutory duties, this can create issues with immigration compliance, leading to delays or refusals in future visa renewals.This is why many businesses rely on professional bookkeeping services in Thailand, including outsourced bookkeeping in Thailand, to maintain their accounts and satisfy Thai bookkeeping and tax compliance standards, and support long-term operational stability.

Bookkeeping Obligations Under Thai Law

All foreign owned companies are required to follow a clear set of bookkeeping and reporting rules. These obligations apply regardless of company size and level of activity (including dormant companies) and need to be maintained consistently.

Corporate Income Tax Calculations and Filings

Companies in Thailand are required to complete annual tax filing requirements, including a half-year corporate income tax (CIT) return (Form PND 51) and a final year-end CIT return (Form PND 50), which must be supported by audited financial statements.

All companies registered in Thailand are required to submit these filings even if they have no activities or no revenue during the year. Thailand does not have a “dormant company” status as in some other jurisdictions, which can sometimes cause confusion for foreign investors.

Non-compliance will result in fines, surcharges, and potential criminal penalties. Under the Revenue Code, company directors can be held personally liable for failure to ensure accurate and timely filings, and may face prosecution in addition to financial penalties imposed on the company.

Mid Year Filing

Companies in Thailand are required to submit a half year Corporate Income Tax return no later than two months after the end of the first six months of their accounting period.

For most companies, the tax is calculated based on 50% of the estimated annual profit. However, certain businesses, including publicly listed companies, banks, and some financial institutions, must calculate tax based on their actual net profit for that six-month period.

The prepaid tax made as part of this filing is creditable against the company’s annual tax liability.

If a company underestimates its annual profit in the half-year tax filing, either intentionally or due to overly cautious forecasting, and the actual year end profit turns out to be more than 25% higher than the estimated amount, then a fine of an additional 20% tax on the difference between the forecasted and actual tax liabilities.

Annual Filings

In Thailand, a company’s tax year generally follows the calendar year, starting on January 1 and ending on December 31. However, businesses may select a different financial year, as long it does not exceed 12 months.

Thailand operates under a self-assessment tax system. This means companies are responsible for accurately preparing and submitting their own tax returns, as well as paying any taxes due, by the required deadlines.

The annual Corporate Income Tax (CIT) return must be filed within 150 days after the end of the company’s financial year. Meeting this deadline is essential to avoid penalties and ensure compliance with the Revenue Department’s regulations.

How Do Companies Complete the Annual Closing

To close the accounts for the financial year, Thai companies must prepare a set of annual financial statements that reflect its business activities and financial performance over the past year.

These financial statements must include:

- Statement of Financial Position (Balance Sheet): Summarizes the company’s assets, liabilities, and equity, offering a snapshot of its financial health.

- Profit and Loss Statement: Details the company’s income, expenses, and net profit or loss for the year.

- Statement of Changes in Equity: Shows changes in shareholder equity, including net profit, dividend distributions, and other adjustments.

- Cash Flow Statement: Tracks the inflow and outflow of cash from operations, investments, and financing activities.

Annual Audit

Once the financial statements have been prepared, they must be audited by an independent auditor.

Independent audits are mandatory in Thailand to verify the accuracy of the financial statements and that they satisfy all the required accounting and financial reporting regulations.

The audit must be conducted by a certified auditor and cannot be performed by the company’s internal accounting team. The accountant in charge of the bookkeeping remains responsible for preparing the final financial statements, coordinating with the auditor, responding to audit queries, providing supporting documentation, and implementing required adjustments until the audit report is issued.

The Annual General Meeting

Under the Thai Companies Act, all companies are required to hold an Annual General Meeting (AGM) at least once per year.

The AGM must take place within four months after the end of the company’s financial year. During this meeting, shareholders review and approve key matters, including the company’s audited financial statements.

The AGM also provides an opportunity for shareholders to review the auditor’s report, raise questions, and request clarification on any financial issues.

Submitting the End of Year Filing

Once the financial statements have been approved at the AGM, the final filing must be submitted to the Ministry of Commerce. This filing must be completed within 1 month of the AGM and the following documents must be submitted:

- Audited financial statement

- Balance sheet

- Company name

- Detail of directors

- List of shareholders

- Minutes of the annual meeting

- Profit and loss accounts

- Type of business

All documents must be prepared in Thai, however, the documents can be prepared in another language along with a Thai translation.

Read more:

How to Complete the Annual Closing Process for Company Accounts

VAT Registration and Monthly VAT Filings

In Thailand, not all businesses are required to register for VAT. However, if a business’s annual turnover exceeds 1.8 million baht, VAT registration becomes a mandatory requirement. Once the turnover threshold has been reached, the company must be registered for VAT.

VAT registration is required for companies that wish to hire foreign employees.

Businesses with an annual turnover below the 1.8 million baht threshold are not required to register for VAT and may benefit from simplified accounting procedures, as they are not obligated to file monthly VAT returns (Form PP.30) with the Revenue Department.

In Thailand, the Value Added Tax (VAT) system has a current rate of 7%, which applies to the majority of goods and services.

However, in Thailand certain goods and services may be exempt from VAT or subject to reduced rates. For example, exports and specific services rendered in Thailand but used abroad are zero rated, meaning they are not subject to VAT charges.

Read more:

VAT Registration in Thailand and When to Register

What is a Company in Thailand’s VAT Obligations?

In Thailand, VAT-registered businesses must file Form PP.30 every month, even with no activity. The deadline is the 15th of the following month for paper filing and the 23rd for online filing, with VAT payable by the same deadline.

If the goods or services are also subject to excise tax, the VAT return must be submitted alongside the excise tax filing to the Excise Department.

Withholding Tax obligations

Withholding Tax (WHT) is considered as one of the most confusing parts of bookkeeping and tax compliance in Thailand for foreign investors. Unlike in many countries, WHT in Thailand is a source based tax that is deducted at the point of payment rather than at year end.

Withholding tax applies to a wide range of payments, including salaries, services, rent, dividends, interest, royalties, and even some cross-border transactions, making it an important consideration for businesses in Thailand.

The confusion around Withholding Tax arises from the different rates and when they are applied. The applicable rate depends on factors such as the type of income, the residency Withholding Tax Obligations.

If you are unsure which rate applies or how withholding tax should be reported, professional accounting services Thailand can review your transactions, confirm the correct treatment, and help you avoid costly filing errors or penalties.

Withholding Tax Obligations

Companies that withhold tax must submit the withholding tax return (PND form) and pay the tax to the Revenue Department by the 7th of the month following payment (extended to the 15th for e-filing). In practice, professional bookkeeping services in Thailand will consolidate all withholding tax payments for the month and submit them together the following month, instead of filing after each individual payment.

Failure to file on time will result in a fine of THB 100 if submitted late but within the same month, or THB 200 if submitted later. In addition, a surcharge of 1.5% per month (or part thereof) is applied to the unpaid tax amount until fully paid.

Read more:

Withholding Tax Thailand, Everything You Need to Know

Withholding Tax Certificate in Thailand: Section 50 Bis

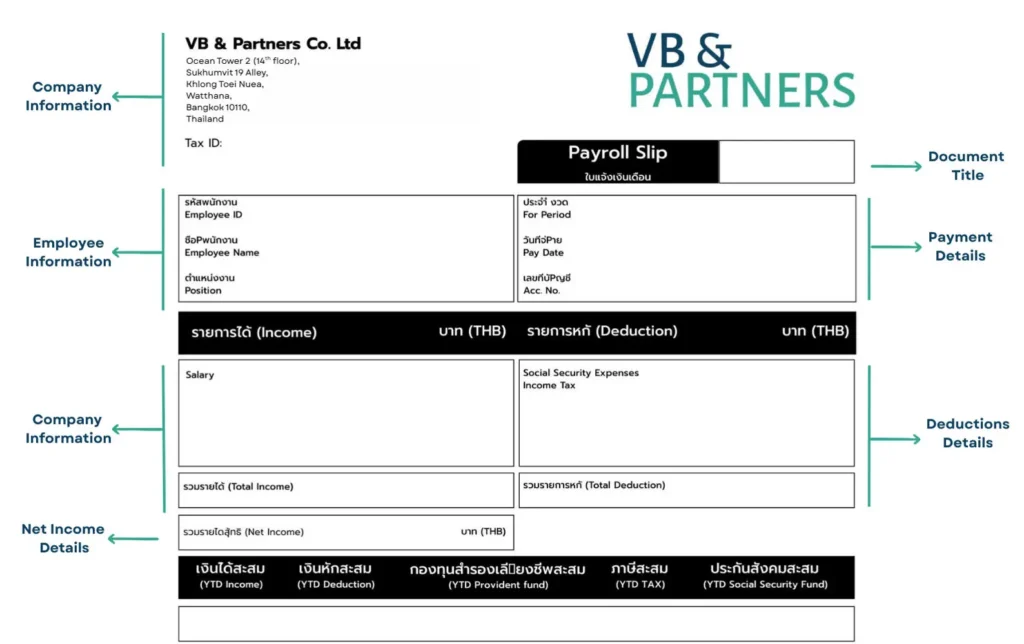

Payroll and Social Security Compliance

For companies with employees, payroll and social security are another mandatory requirement for Thai bookkeeping compliance and bookkeeping.

Under Thai labor law, employers are required to pay their employees at least once per month. For each pay cycle, employers are required to provide their employees with a payslip. Payslips may either be physical or electronic and must include the following details:

- the employee’s earnings,

- deductions, and;

- net pay.

It is important to note that employers are legally required to maintain accurate payroll records for a minimum of seven years.

Payslips

In Thailand, employers are legally required to provide employees with a detailed breakdown of their salary for each pay period (usually monthly). This breakdown can be a physical document issued to the employee or an electronically prepared epayslip.

As per the Labour Protection Act, employers are also required to keep payroll records, including payslips, for at least 7 years.

Read more:

Issuing an Epayslip in 2025: A Payslip Guide for Employers

Social Security Deductions

The following deductions and contributions should also be properly calculated and deducted:

Social Security Fund (SSO)

Both employers and employees are required to contribute 5% of the employee’s monthly salary to the Social Security Fund. The contribution is capped at a maximum of THB 875 per month for each party, resulting in a total maximum Social Security contribution of THB 1,750 per month per employee.

Contributions must be made by the 15th of each month. This fund provides coverage for various benefits, including unemployment, disability, maternity and paternity leave, illness, injury, death, and retirement.

Workmen’s Compensation Fund

Thailand’s Workmen’s Compensation Fund (WCF) provides financial support to employees in the event of work-related injuries, illnesses, disabilities, or death. Employers are required to contribute to this fund annually at rates ranging from 0.2% to 1% of each employee’s annual wages, depending on the assessed risk of the business activity.

The WCF contribution is calculated on annual wages up to THB 240,000 per employee, which means the maximum contribution is between THB 480 and THB 2,400 per year. Employees do not contribute to this fund, as it is entirely funded by the employer.

Employees Provident Fund

The Provident Fund is an optional retirement savings scheme designed to help employees build financial security for the future. Where applicable, contribution rates usually range from 2% to 15% of the employee’s monthly salary.

Employee Welfare Fund (EWF)

The Employee Welfare Fund is a newly introduced program under the Labor Protection Act to provide financial support to employees in cases of termination, resignation, or death.

Starting on the 1st October 2026, all employers in Thailand with 10 or more employees are required to register their staff with the fund, unless they already offer a registered provident fund or a comparable scheme that provides equivalent benefits.

An exemption is available for companies with alternative programs. However, this fund must cover all employees, not just a portion of the workforce.

Managing Deadlines and Penalties

Thailand applies strict deadlines in relation to tax, VAT, payroll, and withholding filings, and these obligations apply equally to all foreign-owned businesses. Late or inaccurate submissions can result in significant penalties. This makes hiring reliable bookkeeping services in Bangkok a highly recommended requirement.

For companies with foreign shareholders or directors, bookkeeping for foreign-owned companies must be maintained continuously throughout the year. Proper Thai bookkeeping compliance helps maintain accurate monthly and annual filings, keeps documentation audit ready, and reduces potential refusals or delays for visa and work permit applications and renewals. Many businesses rely on professional bookkeeping services Thailand or outsourced bookkeeping Thailand to help manage this workload efficiently and consistently.

VB & Partners provides bookkeeping services Thailand supported by a team of experienced accountants. VB & Partners also offers wider accounting services Thailand, to help businesses meet deadlines, manage bookkeeping and tax compliance Thailand, and maintain long-term compliance.

Common Bookkeeping Challenges for Foreign Businesses

Many bookkeeping issues arise from misunderstanding how Thailand’s system works rather than from negligence.

Common challenges include mixing personal and company expenses, incomplete or non-compliant invoices, delayed bookkeeping updates, and incorrect VAT treatment. Another frequent issue is reliance on offshore accountants unfamiliar with Thai standards and filing requirements.

These issues often surface during audits, when corrections are more costly and disruptive.

How Professional Bookkeeping Services Can Help Foreign Investors in Thailand

Professional bookkeeping services can help foreign business owners and investors understand and manage the Thai accounting and bookkeeping requirements. Some of the associated benefits of outsourced bookkeeping in Thailand includes:

Accurate records under Thai standards

Professional bookkeeping maintains accurate monthly records in line with Thai accounting standards and supports proper financial management. All company transactions must be backed by appropriate documentation, typically tax invoices or receipts, with transactions reviewed on an ongoing basis to identify potential issues early. Certain payments are also subject to Withholding Tax, which can be complex for foreign investors.

To remain compliant and maintain effective financial management, companies are required to keep monthly bookkeeping records covering all financial activity, including income, expenses, and other transactions. Proper account management supports smooth and timely monthly and annual submissions and helps reduce the risk of penalties and late filing fees.

These obligations apply equally to companies holding real estate or classified as dormant with little or no activity. Such companies remain subject to the same accounting and tax filing requirements as active operating businesses. Unlike some jurisdictions, Thailand does not provide a dormant status with reduced compliance obligations.

For BOI-promoted companies, or businesses planning to raise capital, secure financing, or sell their operations, properly maintained financial statements are essential. Investors, lenders, and counterparties expect clear, accurate, and well-documented accounts before proceeding with any transaction.

Even if a company is not actively trading, or exists mainly to hold assets such as property, the same bookkeeping and tax rules still apply. For foreign investors, professional bookkeeping and accounting services in Thailand are often the most reliable way to stay compliant without unnecessary risk.

Audit-ready books

As the annual audit is a mandatory requirement for all companies in Thailand, proper preparation is strongly recommended. The audit process follows a strict framework and requires extensive documentation, including accounting records, supporting invoices, and statutory filings.

If the audit is not completed correctly, companies may face penalties of up to THB 200,000. This liability is split between the company itself, which may be fined up to THB 100,000, and the directors personally, who may also be fined up to THB 100,000. In addition, companies that fail to submit properly audited financial statements may attract closer scrutiny from the Revenue Department, including tax audits or additional tax assessments.

Importantly, financial penalties are not the only consequences of failing to complete the annual closing correctly.

Risk of Being Declared Defunct

Failure to meet annual compliance requirements can lead to serious consequences. The Department of Business Development actively monitors registered companies, and prolonged non-compliance may result in removal from the business registry.

Companies that fail to file financial statements for three consecutive years may be struck off, losing their legal status and ability to operate. While court reinstatement is possible within ten years, the process is time-consuming, costly, and complex.

Director Liability and Personal Exposure

Directors may be held personally responsible for annual compliance. Failure to meet these obligations can result in fines, compensation claims, or removal from office.

Key duties related to the annual closing include:

- holding the shareholders’ meeting to approve audited financial statements within four months of the fiscal year end

- filing audited financial statements and supporting documents within one month of the meeting

Where failures involve misconduct, such as falsified filings, directors may also face criminal liability if the offence resulted from their actions or negligence.

Loss of BOI Status and Privileges

For BOI-promoted companies, non-compliance carries additional risk. The Board of Investment closely monitors annual reporting obligations.

Failure to submit annual BOI reports may result in:

- suspension from BOI online systems used for visa and work permit processing

- loss of BOI privileges and incentives

- audits, inspections, and formal warnings

- revocation of the BOI promotion certificate

Once revoked, BOI incentives and tax benefits are permanently lost.

Impact on Work Permits and Visas

Companies must submit filed annual returns and audited financial statements when applying for or renewing Non-Immigrant B visas and work permits.

If these documents are unavailable or incomplete, applications are likely to be rejected. This applies to both standard Thai companies and BOI-promoted entities, and can directly disrupt staffing and operations.

Accurate and well-maintained records create clear audit trails and complete documentation throughout the year, supporting Thai bookkeeping compliance across tax, corporate, and regulatory filings.

Read more:

Missed Your Annual Closing Deadline? Here’s What to Know

Coordinated tax, VAT, and payroll compliance

For many foreign investors, coordinating tax, VAT, withholding tax, and payroll filings in Thailand can be confusing, as each area has different rules, timelines, and documentation standards.

Professional accounting services in Bangkok can help bring these requirements together, allowing accounting records to be used for accurate tax filings, VAT returns, withholding tax submissions, and payroll reporting. This structured approach reduces misalignment, limits filing errors, and supports consistency across all reporting obligations.

Long-term compliance rather than last-minute fixes

One of the biggest advantages of professional bookkeeping is the long-term stability it offers. Properly prepared and structured books that anticipate regulatory and reporting requirements reduce uncertainty, minimise compliance risk, and support consistent operations as a business grows

Our Thoughts

In our experience, bookkeeping is one of the most underestimated risk areas for foreign-owned companies in Thailand. Problems rarely arise from a single mistake, but from patterns of inconsistency over time.

Professional bookkeeping services offer compliance and also protection for directors, support immigration processes, reduce audit exposure, and give management the financial clarity needed to operate confidently.

The best time to structure bookkeeping correctly is at the start of operations. Fixing issues later is always more complex and more costly.

If you want to check that your bookkeeping framework is aligned with Thai regulatory expectations, VB & Partners can review your current records and help structure a system that supports ongoing compliance.

Disclaimer

This information is provided for general informational purposes only and is not legal, tax, or financial advice.