Introduction

Conducting business in Thailand often necessitates travel, whether it’s attending industry events, meeting clients, or overseeing operations in different locations. However, properly budgeting, documenting, and reimbursing these travel expenses can be a complex process, with potential pitfalls companies should be aware of.

As a company operating in Thailand, it’s important to understand the regulations and best practices surrounding travel expense reimbursement to ensure compliance.

Key Points

- Companies in Thailand must prove that travel expenses were incurred for legitimate business purposes and not for personal pleasure. Supporting evidence like emails, invitations, or event brochures should be kept.

- Original receipts/invoices specifying the full name of the company, registered address and tax ID are required for claiming expenses like air tickets, meals, accommodation, and transportation. E-receipts or incomplete receipts may not be accepted by the Revenue Department.

- Daily allowances provided to employees for meals and transportation are generally considered part of their income and subject to personal income tax, unless the employee travel reimburses the exact expenses with receipts.

- Certain travel expenses, such as car rental costs, have specific limits set by the Revenue Department beyond which they cannot be claimed as deductible expenses.

- Failure to provide proper documentation or include disallowed expenses (add-back expenses) in the tax return can lead to additional tax liabilities and penalties from the Revenue Department.

Can Companies Claim Travel Expenses in Thailand?

In the event of an investigation by the Revenue Department Of the company’s accounts, the Revenue Department will check the books of your company, and consider any claimed expenses accordingly. In relation to any expenses claimed for travelling, they will typically assume that the trip was for pleasure rather than for business.

Therefore, the company will have to prove that the trip was for company business and that all the expenses paid on the trip were reasonable for the trip and reimbursed at cost. If the company cannot prove these 2 key points, the travelling expenses claimed could be added back to your bottom line profit and therefore, the company will have to recalculate the corporate income tax and possibly have to pay more tax.

How can Companies Prove the Trip Was for Business Purposes?

In order to prove that the trip was for the company business and not for pleasure, companies must attach some evidence such as email correspondence with, or invitation from, the company/client in the country (or province if within Thailand) where the business trip was to take place.

Please note that things such as trade show brochures or other relevant publications can be submitted as proof if you went to that particular country for that specific event. Companies should include such supporting documents to the payment voucher in which you are travel reimbursed for the travelling expenses.

How Do You Claim Travel Expenses?

In order for the employee and the company to be able to claim their travel expenses as deductible expenses, including lodging costs, they must be able to prove that the expenses submitted for the trip are legitimate expenses. In practice, the general rule is that you need to have original receipts/invoices for each expense item specifying the company’s full name, registered address and Tax ID. It may not be possible to obtain such documents for some expenses e.g.taxi fares or food from small business owners. In this case, a normal receipt can be submitted as the amount remains reasonable (no more than 1,000 baht).

In countries outside of Thailand where it is not common to issue a receipt with the full name of the company, then the receipt with supporting evidence of the trip (and flight tickets and hotels booked with proper receipt with company name on it) may be acceptable

Air Tickets

In practice, the safest way to ensure an air ticket can be claimed is to purchase a ticket through a travel agent based in Thailand. Thai travel agents will be able to issue an invoice in your company’s name.

If the use of an agent is not possible and the ticket was bought online or it is not possible to get a receipt issued in your company’s name, then the E-receipt from the vendor may suffice. Please note, there is no guarantee that an e-receipt will be accepted by the Revenue Department in the event of an investigation. Acceptance is entirely dependent upon the officer who is reviewing the documentation.’

Meals and Accommodation

In order to be able to claim the costs of the meals and lodging incurred during a business trip, the Revenue Department will require receipts for each of those expenses from the vendors, making proper budgeting essential. In practice, the receipts should be in the company’s name. However, should the expenses be incurred overseas it may not be possible to use the company’s name and an invoice made out to the employee should suffice.

Taxi Fares and any similar expenses

In situations where vendors do not issue receipts to their customers e.g taxis, public transport etc, then the travelling expense report (or expense reimbursement form) should clearly specify the reason why the expense was required.

For example, for taxi fares, the expenses report should clearly explain why the use of a taxi was required, from where to where the taxi journey was and for what purpose the business trip was made.

Car Rental

Should a car be rented for the duration of the business trip, the expense can be claimed as a deductible expense. However, only rentals satisfying the following criteria can be claimed:

- The rental cost of a passenger car or a bus (with a maximum of 10 seats for passengers) must not exceed 36,000 THB including VAT per month per car for monthly or yearly rentals.

- Daily car rentals must not exceed 1,200 THB including VAT per day per car.

Daily Allowances

Often companies will provide their employees with a daily allowance for expenses such as meals and taxi journeys, as outlined in their travel policy. In such a situation, the allowances will in practice be considered as part of the employee’s income and therefore will need to be included in their personal income tax calculation. However, if the employee reimburses for the expenses at cost, it will not be part of his income.

What Happens if you do not Have Receipts or Invoices for the Expenses?

If it is not possible to provide receipts or invoices for the claimed travel expenses, then the accountant will not be able to book this as expenses and/or the auditor may raise this point. In the event of an investigation, the Revenue Department officials will very likely add them back to recalculate the corporate income tax.

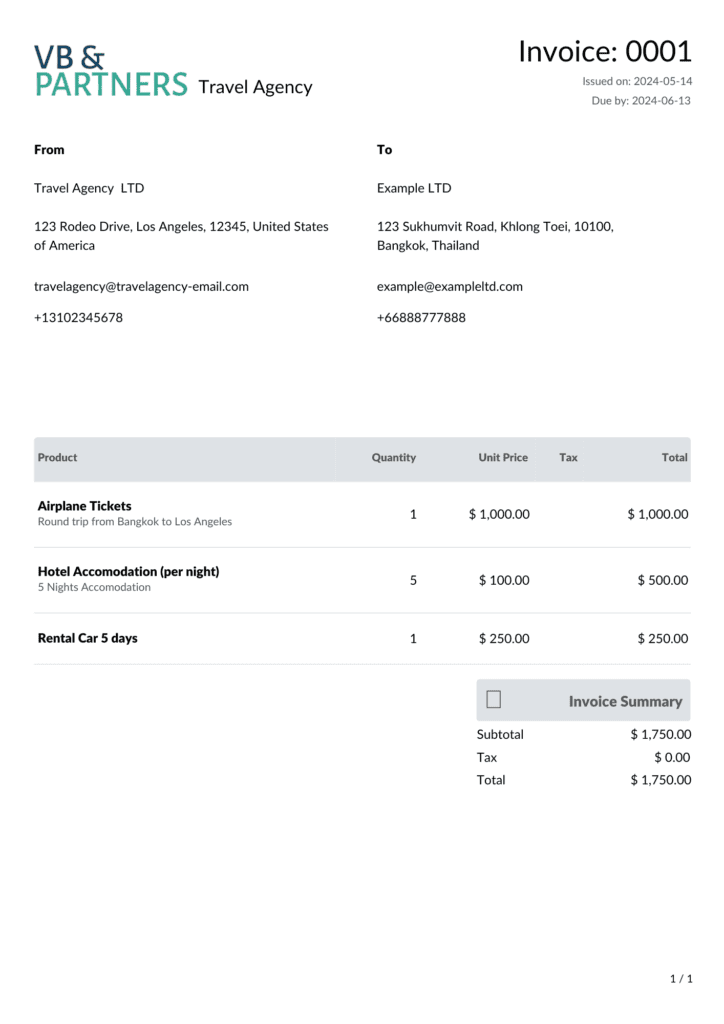

Example Invoices

Please see below for an example of an invoice which would can be used as a deductible travel expense:

This invoice can be used to claim back the travel expenses as it clearly displays the following information:

- the company’s full name,

- registered address

Please note, the Tax ID is only necessary if the payor is a Thai company registered with the VAT to claim back the VAT.

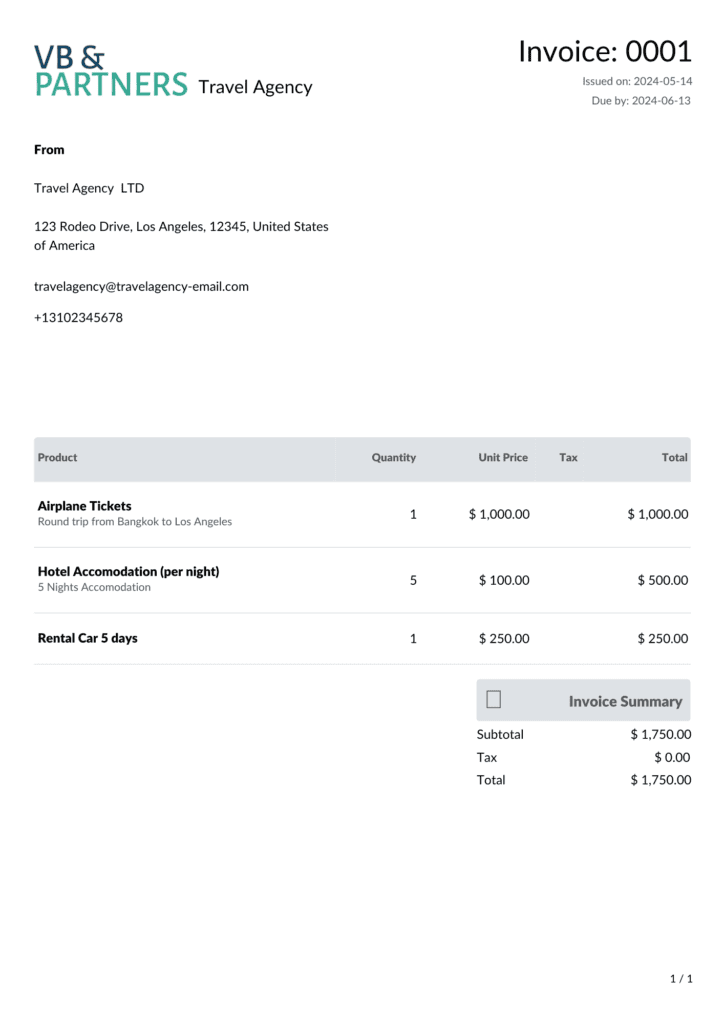

The following is an example of an invoice that would not be eligible to be submitted as a travel expense.

This invoice may not be acceptable as it does not include the required company name and registered address. Furthermore, the value of the transaction is too high to be considered as a petty cash transaction.

What are Add Back Expenses?

Add-back expenses refer to the expenses that are included in a company’s accounting records but are not allowed as deductions in the calculation of net profits for tax purposes. The Thai Revenue Code, specifically Section 65 Ter, outlines the expenses that cannot be claimed as deductions. These expenses need to be added back to the profits in the tax return.

Failing to add back these expenses in the tax return can lead to inaccuracies and potential penalties from the Revenue Department.

Why Does My Accountant Not Want to Book Travelling Expenses?

When looking to claim travelling expenses from your company in Thailand you are supposed to provide supporting documents, normally invoices, to your account. These invoices should contain the correct information, such as the company name and registered address. However, if it is not possible to provide these detailed invoices, the accountant may ask for additional supporting documents. If it is not possible to provide these additional documents, the accountant may refuse to accept them as expenses.

It is important that the expenses claimed are in order and correctly filed because at the end of the year, all Thai companies are subject to an audit from an external auditor. While some auditors may be more relaxed than others when it comes to the audit and expenses, this doesn’t mean the company won’t be investigated by the Revenue Department.

It is also important to note, that if claims which don’t satisfy the requirements are accepted by the company’s accountant, an auditor who properly performs the yearly audit will flag such an expense and either ask for the content to be revised or make a note in his report that an unsatisfactory claim was made.

Our Thoughts

Thailand has a strict policy for deductible expenses and what can be claimed, especially for travel expenses. This can be problematic for companies who need to undertake business related travel on a regular basis.

However, the strict policy for travel expenses is not the case in all jurisdictions. In fact, it is actually a common occurrence for businesses to have another company in a more liberal jurisdiction such as Hong Kong. Having an entity in Hong Kong would allow companies to claim their travel expenses there rather than in Hong Kong, allowing them more freedom for their claims and deductions.