TL;DR BOI accounting requirements are much more complex for BOI promoted companies compared to a regular Thai company. Foreign investors who have obtained a BOI promotion in Thailand must follow additional reporting, tax, and compliance rules linked to their BOI promotion. This includes separating promoted and non-promoted activities, tracking fixed assets correctly, filing progress reports on time, and maintaining records that support tax benefits and audit readiness. Working with an accountant who understands BOI requirements helps reduce compliance risk and protect your promotion status.

Introduction

For companies that have received Board of Investment (BOI) promotion, many of the restrictions that are often faced by foreign business owners are removed. For example, a BOI company in Thailand can be 100% foreign owned and to carry out activities that would otherwise be restricted under Thai law.

However, the responsibilities of a BOI promoted company do not end once the application process is complete. BOI companies remain subject to ongoing reporting obligations, compliance requirements, and specific accounting standards.

While it is often assumed that the accounting requirements for a BOI promoted company are the same as those for a regular Thai company, this is not the case. In addition to the standard statutory obligations, BOI companies are subject to additional reporting and accounting requirements as well.

Failure to properly manage these obligations can have significant consequences for both the business and its foreign investors. Examples include the loss of BOI promotion status, repayment of benefits previously received such as BOI tax benefits, and potential issues with the renewal or continuation of visas and work permits for foreign employees.

This guide explains the obligations BOI companies must fulfil to retain their promoted status. From regular progress reports to specific company accounting practices, understanding BOI accounting is essential for smooth operations and continued BOI support.

Key Points

- BOI companies face stricter accounting obligations than regular Thai companies, including additional reporting requirements, project progress reports, and a mandatory financial audit after three years.

- BOI Promoted and non-promoted business activities must be kept strictly separate in accounting records, issuing tax-exempt invoices for activities outside the BOI-approved scope can trigger a Revenue Department audit and potential loss of benefits.

- BOI companies must invest at least THB 1 million in qualifying fixed assets, though the BOI’s definition of what counts as a fixed asset differs from standard Thai accounting rules, making correct classification important.

- Missing reporting deadlines carries serious consequences, including suspension of tax incentives, loss of BOI promotion status, and potential repayment of all tax benefits previously received.

What Makes BOI Accounting Different from Regular Thai Company Accounting?

Companies that have received a BOI promotion are entitled to a range of incentives that can significantly reduce the challenges often faced by foreign investors in Thailand. A BOI company Thailand may benefit from 100% foreign ownership, permission to operate restricted or promoted activities under the Investment Promotion Act, as well as tax and non-tax incentives designed to support long-term investment.

However, due to the significant advantages and removal of restrictions, BOI companies are subject to increased scrutiny from the BOI and other government bodies such as the Revenue Department. Continued access to any benefits that have been awarded to a promoted company is dependent on proper BOI accounting and ongoing compliance.

Keeping clear and accurate BOI accounting records is essential to retain eligibility for incentives and to comply with the reporting requirements that apply to promoted companies. It is also highly important for companies that have received a BOI promotion to work with an accountant who is familiar with BOI regulations and the specific accounting requirements required of promoted businesses.

What are the Accounting Requirements for all Thai Companies?

Understanding annual and monthly accounting requirements is essential for any company operating in Thailand, whether BOI-promoted or not. Thai companies are subject to a standard framework of corporate income tax filings, audited financial statements, shareholder approvals, and ongoing monthly tax obligations. Failure to properly complete these requirements can result in penalties, financial exposure, and increased scrutiny from the authorities.

Annual Accounting Requirements for Thai Companies

In Thailand, a company’s tax year typically runs from January 1 to December 31. However, a company may choose a different financial year, as long as it does not exceed 12 months.

Thailand operates a self-assessment tax system, where companies are responsible for preparing and filing their tax returns in Thailand by the required deadlines while paying any taxes due. The annual Corporate Income Tax (CIT) in Thailand return must be filed within 150 days of the end of the accounting period.

To close the fiscal year, a company in Thailand must prepare written financial statements summarising its business activities and financial performance for the year.

These financial statements must be audited by an independent certified auditor and submitted to the Ministry of Commerce within 150 days from the end of the financial year. The audit verifies the accuracy of the accounts and confirms compliance with Thai financial reporting regulations. It cannot be conducted by the company’s internal accounting team.

In addition, every company is required to hold an Annual General Meeting as per the Thai Civil and Commercial Code. The AGM must take place within four months of the financial year end. During the meeting, shareholders review and approve the audited financial statements and may question the auditor’s report or request further clarification on the company’s financial position.

Once the financial statements have been approved at the AGM, the final filing must be submitted to the Ministry of Commerce. This filing must be completed within 1 month of the AGM.

Read more:

How to Complete the Annual Closing Process for Company Accounts

Monthly Accounting Requirements for Thai Companies

The following is a general outline of what all BOI and Non-BOI promoted companies should prepare each month with regards to the monthly accounting and tax filings.

The standard monthly tax filing process includes:

- Withholding tax filings:

- Form PND 3 (individuals)

- Form PND 53 (companies)

- Form PND 54 (foreign payments)

- VAT filings (if registered):

- Form PP30 (monthly VAT)

- Form PP36 (self-assessed VAT on foreign services)

Important Tax Rates and Deadlines For Your Company

| Type of Tax | Rate of Tax | Due Dates for Payment of Tax |

| Corporate Income Tax (CIT) | Standard Rate: 20% SME Rate: SMEs with annual sales not exceeding 30 million baht and paid-up share capital not exceeding 5 million baht are eligible for the following reduced tax rates: 0% for net profits up to THB 300,000, 15% for net profits between THB 300,001 and THB 3 million, and; 20% for net profits exceeding THB 3 million | CIT Half year Return Due Date: Within 150 days from the closing date of the accounting period (Due within two months after the end of the first six months of the accounting period (e.g., by 31 August for companies with a year-end of 31 December). CIT Final Payment Due Date: Within 150 days from the closing date of the accounting period (e.g., by 30 May for companies with a year-end of 31 December) |

| Monthly Withholding Tax (WHT) from Employee Salaries | Between 0 and 35% (Progressive Scale) This is the personal income tax of the employee withheld at source by the employer from the employee’s gross salary. | Payment to be made to the Revenue Department by the 7th of the following month (15th if filed electronically) |

| Social Security Office (SSO) Contributions | 5% of employee’s wage withheld from the employee salary (capped at THB 750 per month) And Employers are required to contribute 5% of each employee’s monthly wage to the Social Security Fund, capped at a maximum of THB 750 per employee per month. Please note, the Social Security contribution in Thailand is capped at 1,500 baht per employee per month. | Payment to be made to the SSO by the 15th of the following month |

| Value Added Tax (VAT) | 7% | Payment to be made on or before the 15th day of the following month in which the payment was made and the issuing of the tax invoice. |

| Withholding Tax (WHT) on payment for certain services | 0-15% | Payment to be made on or before the 7th day of the following month in which the payment was made. |

What are the additional BOI Accounting in Thailand Requirements?

Obtaining BOI promotion provides companies with access to significant incentives and benefits. However, it also places the company under additional reporting and compliance obligations, including:

BOI Reporting

BOI promoted companies are required to regularly update the BOI on their progress. Regular progress reports are due on specific intervals:

- 6 months: Confirm project implementation has begun.

- 1 year and 2 years: Provide updates on project progress.

These reports are required to show the BOI that the project aligns with the approved BOI promotion.

After 3 years the project will also be required to complete an audit of the company’s financial statements by an approved auditor. This audit confirms compliance with BOI conditions and tax benefits claimed.

Other Project Deadlines:

- Within 30 months: The project must import machinery and equipment.

- Within 36 months: The project, including construction, machinery installation, and factory readiness, must be completed.

- Extensions can be requested with justification.

- Annual Reports : Every year by July 31st, submit a report outlining financial status and project operation results.

BOI Accounting Requirements

BOI promotion can grant access to highly valuable incentives, including permission for up to 100% foreign ownership and corporate income tax exemptions. Foreign owned companies can undertake activities in sectors that would otherwise be restricted under the Foreign Business Act, this allows foreign-owned companies to operate on similar terms to Thai-owned businesses. As a result, BOI status can have a significant effect on market competition. In exchange for these advantages, promoted companies are subject to stricter reporting and compliance obligations.

One area that is commonly subject to increased scrutiny is the company’s accounting records. For BOI-promoted companies, the accountant must maintain accurate and up-to-date books and tax filings at all times.

BOI-promoted companies are often granted tax incentives (with the exception of TISO promotions), which means close care and attention must be taken when issuing invoices. Any goods or services invoiced under a tax exemption must fall strictly within the scope of the BOI promotion and promoted activities, where applicable, within the scope of the company’s foreign business licence or certificate.

If an invoice relates to activities outside the approved scope, the company may face a tax audit and potential tax reassessment, including penalties and surcharges. This is particularly important for a company that carries out both promoted and non-promoted activities, as not all operations will qualify for incentives.

For invoiced services or goods outside the BOI-approved scope, the company must maintain separate accounting records and account for corporate income tax on those activities.

If a BOI-promoted company fails to satisfy these conditions, the BOI may issue a formal warning notice. Where no valid reason for the failure can be provided, the BOI can recommend to the Board that the promotion be revoked.

If the promotion is withdrawn, the company may be required to repay any tax benefits previously granted, on a retroactive basis, as if the promotion had never been awarded.

What Are the BOI Accounting Requirements for Fixed Assets?

As part of the requirements for their approval, BOI-promoted companies are required to invest at least THB 1 million in fixed assets, also known as investment capital. While this may appear straightforward, the BOI’s interpretation of what qualifies as a fixed asset can vary.

It is important to note that the BOI’s definition of qualifying fixed assets does not necessarily match with standard Thai accounting definitions. Assets that would usually be capitalised under Thai Accounting Standards may not count towards the BOI investment threshold, and vice versa. This difference is one that many accountants may not be familiar with, and misclassification at this stage can have significant consequences for the overall BOI assessment.

For BOI assessment purposes, fixed assets will usually exclude the cost of land and working capital. It is therefore important to correctly classify qualifying assets at an early stage, as misclassification can affect both the approved investment amount and the scope of incentives granted.

Accurate identification and proper recording of these investments is also required to satisfy the condition and obtain final confirmation following the BOI three-year review.

In addition, certain BOI promotions are granted subject to specific investment conditions. These requirements must be carefully tracked and properly reflected in the company’s accounting records to demonstrate ongoing compliance.

Some BOI promotions also require minimum expenditure requirements within specific asset or cost categories. For example, a promotion may require a minimum investment in machinery of a particular type, or a minimum spend on research and development activities or hiring a certain number of Thai employees (within a specialist field or skill) that satisfies a minimum salary requirement).

Where these category-specific conditions apply, the accountant must ensure that each expense is properly recorded under the correct accounting classification. This is not just internal bookkeeping. The BOI will review the company’s audited financial statements when assessing whether these conditions have been met, and any discrepancy between actual expenditure and the required categories can result in the condition being considered unsatisfied, even where the total investment figure is otherwise sufficient.

What are Considered as Fixed Assets?

The BOI has a varied approach to classifying fixed assets. The following are examples of what is usually considered as a fixed asset.

Machinery and Equipment: This is the most common category and includes production machinery, tools, and specialized equipment that will be directly used for the promoted activity.

The BOI generally requires new machinery. If you use imported machinery, it must meet specific age criteria (usually under 5–10 years) and requires an efficiency certificate to be counted toward your investment value.

Construction Costs: Expenses for building factories, warehouses, or office buildings directly related to the project.

Infrastructure & Facilities: Costs for installing essential systems like electricity, water supply, and environmental protection systems.

Leasehold Improvements: If you are renting a space, structural renovations (partitions, wiring, flooring) can often be capitalized as fixed assets, provided they have a useful life exceeding one year.

How to Record Fixed Assets to Meet BOI Accounting Requirements

Booking fixed assets for the BOI requires a clear split between promoted and non-promoted activities in the company’s accounting records. Assets, particularly imported machinery and equipment, must be recorded at actual cost, with any import duty exemptions properly reflected.

A fixed asset register will also be required for annual audits and BOI performance reporting.

How to Record BOI Fixed Assets:

Separation of Accounts

Maintain separate fixed asset accounts in the general ledger for BOI-promoted projects. This allows depreciation, tax privileges, and investment thresholds to be monitored independently from non-promoted activities.

Asset Valuation

Record fixed assets at cost, reflecting applicable import duty and VAT treatment in accordance with BOI approval. Any exemptions granted must be traceable to supporting documentation and the approved project scope.

Fixed Asset Register

Maintain a detailed register for each asset, including the BOI certificate number, acquisition date, cost, depreciation rate, and physical location. This register will be used for future audits and compliance reviews.

Category-Specific Expenditure Tracking

Where a BOI promotion imposes minimum expenditure conditions within specific asset or cost categories, each qualifying expense must be recorded under the correct category in the accounting records. Expenses that are incorrectly booked, even if they qualify as fixed assets overall, may not be counted towards a category-specific condition during the BOI’s review of audited financial statements.

Depreciation

Calculate depreciation in line with Thai Accounting Standards, based on the asset’s useful life. Where BOI-specific conditions apply, these must be reconciled against Revenue Department rules.

Reporting Obligations

All fixed asset data must be accurately reflected in the annual performance report submitted to the BOI. Discrepancies between accounting records and reported investment figures may trigger an audit or review.

Supporting Documentation Typically Required:

- Import entry forms and commercial invoices indicating BOI tax exemption status

- A complete fixed asset register

- Depreciation schedules by asset

- The BOI promotion certificate for verification of approved assets

What BOI Tax Benefits Do I Actually Get and How Long Do They Last?

BOI benefits and incentives are often the main reason foreign investors apply for promotion. However, the duration and calculation of these incentives depend on the approved activity category and the specific investment conditions attached to the project.

Tax incentives are not available for all business activities. The length of any corporate income tax exemption depends on the specific promoted activity category and the conditions attached to the approval. In some cases, additional benefits may apply, for example where the project is located in a designated special economic zone, subject to meeting the relevant criteria.

In addition to tax benefits, non-tax benefits remain available for as long as the company maintains its BOI-promoted status. These include 100 percent foreign ownership and reduced requirements for visas and work permits for foreign employees. If promotion conditions are not met or reporting obligations are not properly managed, these privileges may be revoked.

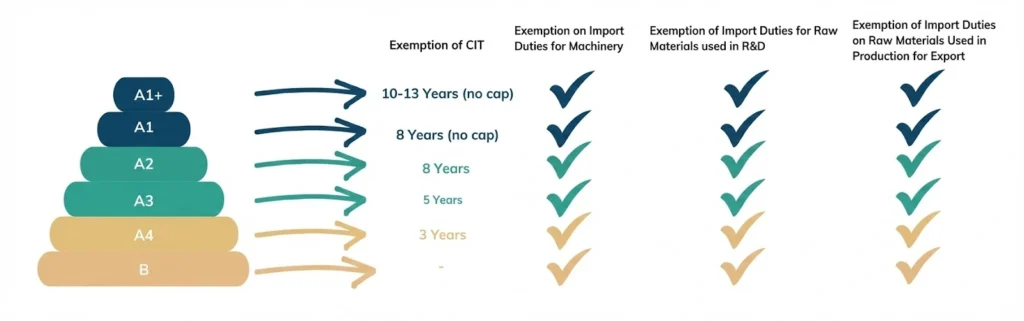

Corporate Income Tax and Other Tax Exemption Periods by Activity Group

The BOI grants corporate income tax exemptions for up to 13 years, depending on the nature of the business and its location. For businesses located in industrial estates or promoted industrial zones, an additional year of corporate income tax exemption is granted. Companies situated in “Investment Promotion Zones” receive three extra years of tax exemption.

Please note, not all BOI promotions are awarded CIT exemptions and the length of the corporate income tax exemption awarded to a BOI promotion depends on the activity of the business and the promotion awarded by the BOI.

Import Duty Exemptions

Exemption from import duties on machinery and raw materials necessary for manufacturing export products for one year, which can be extended.

When Does the BOI Tax Benefits Period Actually Start for a BOI Company in Thailand?

The period during which a project is granted corporate income tax exemption does not begin on the date the promotion certificate is issued by the BOI company in Thailand. In most cases, the exemption period commences from the date the project first generates revenue and first issues an invoice.

An exception applies to projects promoted under the Production Efficiency Enhancement measures. In these cases, the corporate income tax exemption period is calculated from the date the promotion certificate is issued, regardless of when revenue is first generated.

Understanding the applicable commencement date is important when forecasting tax planning and cash flow as a BOI company in Thailand, as the timing directly affects the effective value of the incentive.

Additional Tax Benefits Beyond CIT Exemption

Other BOI tax benefits may apply depending on the approved activity and the specific conditions stipulated by the BOI when awarding the promotion.

Import Duty Incentives

A BOI company Thailand may receive import duty reductions or exemptions on machinery required for the promoted activity. In addition, raw materials imported for use in manufacturing export products may qualify for import duty exemption for one year, with possible extensions subject to approval.

Corporate Income Tax Incentives

In certain activity categories, a 50 percent reduction of corporate income tax may apply for up to five years after the main tax exemption period ends..

Additional merit-based incentives may also apply. Projects that invest in research and development, advanced technology, or productivity improvements may be granted an additional one to three years of corporate income tax exemption, subject to meeting the BOI’s requirements.

Dividend Treatment

Dividends paid from profits generated during the corporate income tax exemption period are generally exempt from income tax if distributed during the tax exemption period or within six months following its expiry.

As the availability and duration of each tax exemption period depend on the approved activity group and investment conditions, careful planning is required to maximise the overall value of BOI tax benefits.

What Reports Do BOI Companies Need to Submit and When Are the Deadlines?

Missing a BOI reporting deadline can lead to delayed approvals, suspension of incentives, or in serious cases, revocation of your entire BOI promotion. BOI-promoted companies are subject to specific BOI compliance requirements that regular Thai companies are not subject to. In practice, BOI reporting obligations require separate filings to the BOI and to the Revenue Department under different timelines.

BOI Progress Reports via E-Monitoring System

As part of the conditions imposed on newly promoted BOI companies are required to submit regular progress reports to show that the company is

The BOI compliance requirements for companies are as follows:

- BOI reporting requires newly promoted companies to submit project progress reports to the BOI after the following periods to ensure that the project aligns with the approved BOI promotion:

- 6 months: Confirm project implementation is ongoing.

- 1 year and 2 years: Provide updates on project progress.

- After 3 years the project will be subject to an audit of the company’s financial statements by an approved auditor. This audit verifies compliance with BOI conditions and tax benefits claimed.

The progress report is one of the main ways the BOI monitors promoted projects. It allows the BOI to review whether the company is developing the project in line with the approved business scope, and incentive conditions.

The BOI will use this report to examine key details such as capital investment, machinery purchases, operational progress, and whether the company is meeting its approved objectives. These reports are basically a way to confirm that the company continues to meet its BOI compliance requirements.

If the report is not submitted on time, the BOI may issue a warning letter. Continued failure to submit the reports can result in delays to approvals, suspension of benefits, or even termination of incentives, including tax privileges.

BOI-promoted companies must file their progress reports through the BOI e-monitoring system, which is the official platform for BOI reporting.

When Do Progress Reports Stop Being Required?

Once a BOI-promoted company reaches full operation, BOI reporting is no longer required and therefore the company is no longer required to submit progress reports.

Full operation means that the company has completed its approved investment, complied with the conditions set out in the promotion certificate, and is operating in line with the approved business scope.

At this stage, the BOI considers that the project has been fully implemented as proposed and no longer requires ongoing BOI reporting requirements.

The deadline for promoted companies to reach full operation status is three years from the date the BOI certificate is issued.

If it is not possible to meet these deadlines, certain extensions may be available depending on the nature of the business:

- Software businesses that do not involve machinery importation may request a one-time extension of up to one additional year.

- Manufacturing businesses may apply for an extension linked to the machinery importation period, with the total implementation period extending up to 6 years.

If a company fails to achieve full operational status within the permitted timeframe, it may face compliance issues or potential loss of their promotion status and associated incentives.

Revenue Department Tax Filings for BOI Companies

Even with a BOI promotion, the company must still follow the standard Revenue Department filing calendar. BOI incentives may reduce tax liability, but they do not remove mandatory filing duties. In practice, most compliance issues arise not because tax is owed, but because filings are late, incomplete, or inconsistent with the company’s supporting documents.

Accounting obligations for all companies in Thailand

Monthly VAT (if VAT-registered):

PP30 (monthly VAT return) and PP36 (self-assessed VAT on foreign services used in Thailand) are due by the 15th of the following month.

Filing is required even if there are no transactions (a “nil” return). Any VAT due must be paid by the same deadline.

Withholding tax:

PND 1 (employee salary withholding), PND 3 (payments to individuals), and PND 53 (payments to companies) are due by the 7th of the following month (or by the 15th if filed online).

Where withholding applies, the company must also issue the relevant withholding tax certificates, as these are often requested by vendors and may be reviewed during audits.

Mid-year corporate income tax:

PND 51 (half-year corporate income tax return) is due within 2 months after the end of the first 6 months of the accounting period.

This is typically based on an estimate of annual profit, and the payment made is credited against the year-end corporate tax position.

Annual corporate income tax:

PND 50 (year-end corporate income tax return) is due within 150 days after the fiscal year-end, together with the audited financial statements.

Read more:

How to Complete the Annual Closing Process for Company Accounts

For BOI companies, the year-end filing also depends on correct accounting treatment, including clear separation of BOI-promoted and non-promoted income where relevant.

How Do I Choose an Accountant Who Understands BOI Requirements?

An accountant who understands BOI requirements is highly recommended for a BOI company in Thailand due to the specific accounting and reporting regulation they are subject to. BOI promotions also come with enhanced scrutiny, structured reporting obligations, and strict conditions around revenue, fixed assets, and tax incentives.

Not all accounting firms in Thailand have genuine BOI expertise. Many general bookkeepers treat BOI-promoted companies as ordinary businesses, which can create risks during audits or when claiming tax exemptions. Common issues include incorrect accounting entries, failure to separate corporate income tax-exempt activities from non-promoted activities, and a lack of understanding of specific BOI reporting requirements.

What BOI Accounting Expertise Actually Looks Like

Proper BOI accounting requires more than preparing monthly tax filings. It requires a technical understanding of how BOI conditions differ with Thai accounting standards and Revenue Department requirements.

A qualified BOI accountant should also be able to explain how revenue must align with the promoted activity, how fixed assets are classified for BOI purposes, and how tax exemption caps are tracked and maintained.

Key qualifications to look for include:

- Active membership with the federation of accounting professions (FAP)

- Experience working with BOI-approved auditor requirements

- Practical knowledge of project-based accounting separation

- Clear understanding of specific BOI activity categories and their conditions

- Familiarity with the BOI e-Monitoring reporting system

Why VB and Partners Specializes in BOI Company Accounting

Our team works fully in English, French, and Thai, which allows us to communicate clearly with foreign directors while coordinating directly with BOI officials where necessary. This removes the communication gaps that often arise when technical BOI matters are handled only in Thai.

Our accountants are also licensed members of the Federation of Accounting Professions and have a demonstrated track record in BOI compliance.

From the very beginning, our experts will help prepare companies for the three-year BOI audit by reviewing fixed asset classifications, monitoring investment milestones, and maintaining supporting documentation in line with BOI conditions. We also set up the accounting systems to properly separate promoted and non-promoted activities, so revenue allocation and corporate income tax treatment are accurate from day one.

Our approach to BOI accounting is built on structure, documentation, and audit preparedness, rather than correcting issues after they arise.

Frequently Asked Questions About BOI Accounting Requirements

Q1: Do all BOI companies need to hire a specialized BOI accountant?

A: While not a mandatory requirement, it is highly recommended. Companies that have received BOI promotion must ensure their accountant is familiar with BOI regulations and accounting requirements. Regular Thai accountants often lack experience with project-based accounting separation, fixed asset classification rules specific to BOI, and the difference between promoted and non-promoted activity tracking.

Q2: Can I use the same accounting software for BOI and non-BOI activities?

A: Yes, but it must be configured correctly with project-based accounting. You need a separate chart of accounts, revenue tracking, and expense allocation for each BOI promotion.

Q3: What happens if my BOI company hasn’t reached the 1 million THB fixed asset requirement yet?

A: Proper accounting of fixed assets with minimum 1 million Thai Baht is important for BOI confirmation. You have until your 3-year BOI audit to meet this requirement, but every fixed asset purchase must be documented correctly from the start.

Q4: When exactly do I need to submit BOI progress reports?

A: BOI promoted companies must submit project progress reports to the BOI at specific intervals:

6 months: Confirm project implementation is ongoing.

1 year and 2 years: Provide updates on project progress.

After 3 years the project will be subject to an audit of the company’s financial statements by an approved auditor. This audit verifies compliance with BOI conditions and tax benefits claimed.

Q5: Can I start claiming BOI tax benefits immediately after receiving my promotion certificate?

A: No. The exemption period begins from the date of the project’s first revenue (first issued invoice), not from the date the promotion certificate is issued. This means you can strategically time when you start operations to maximize your tax benefit period.

Q6: What’s included in VBA Partners’ BOI accounting service?

A: Our all-inclusive BOI accounting package includes: monthly bookkeeping with promoted/non-promoted activity separation, all VAT and withholding tax filings (PorPor 30, 36, PorNgorDor 1, 3, 53), corporate income tax filing with BOI exemption applications, semi-annual February/July e-Monitoring progress reports, 3-year BOI audit coordination and preparation, fixed asset investment tracking against 1 million THB requirement, tax exemption cap monitoring, bilingual English/Thai support via LINE/WhatsApp, and client ownership of accounting software license. From 6,500 THB/month.

Q7 What are the penalties if I make mistakes in BOI accounting?

A: Failure to properly complete accounting requirements can lead to delayed approvals, tax audits, or discontinuation of BOI benefits. Specific issues include: issuing tax-exempt invoices for non-promoted activities (triggers Revenue Department audit), missing progress report deadlines (can terminate BOI status), failing to segregate promoted/non-promoted profits (forfeits tax exemptions), and not meeting 1 million THB fixed asset requirement (BOI confirmation denied).

Q8: Can I lose my BOI tax benefits if my accounting isn’t compliant?

A: Yes. Failure to properly complete accounting requirements can lead to delayed approvals, tax audits, or even discontinuation of BOI benefits. The most common reasons BOI benefits are withdrawn include: failure to submit timely progress reports, incorrect separation of promoted and non-promoted activities, issuing tax-exempt invoices outside BOI scope, not meeting investment commitments shown in accounting records, and missing the 120-day deadline for annual CIT exemption applications. These are all preventable with proper BOI accounting expertise.

Q9: Do I need separate bank accounts for BOI and non-BOI activities?

A: Not legally required, but highly recommended for smoother accounting. Many BOI companies maintain one bank account but use detailed internal tracking to allocate revenues and expenses.

Get Expert BOI Accounting Support from VB & Partners

BOI accounting requirements in Thailand are technical and strictly monitored. Project separation, fixed asset tracking, e-Monitoring progress reporting, and corporate income tax exemption applications all require specialised expertise. A single missed deadline or incorrectly classified transaction can jeopardise valuable tax incentives.

Relying on general accountants who are not familiar with BOI regulations can expose your BOI company to unnecessary compliance risks and potentially costly mistakes.

VB and Partners provides dedicated BOI accounting support for foreign investors operating in Thailand. Our bilingual team works in English, French, and Thai and assists clients with the full scope of BOI accounting obligations from monthly bookkeeping and BOI-compliant financial reporting to preparation for the three-year BOI audit.

Companies operating under BOI promotion benefit from working with accountants who understand the specific reporting framework and compliance expectations of the Board of Investment.

If you would like to better understand the accounting obligations applicable to your BOI-promoted company, our team remains available to discuss your situation and provide practical guidance.

Disclaimer

This information is provided for general informational purposes only and is not legal, tax, or financial advice.